In recent trading, Tenet Healthcare has faced pressure as investors reacted to February’s US jobs report showing unexpected employment contraction and substantial healthcare sector job losses, raising concerns about a potential economic slowdown and weaker demand for medical services.

These macroeconomic worries are emerging just as Tenet prepares to showcase its diversified care delivery network, including its large ambulatory surgery platform, at the Barclays Global Healthcare Conference, highlighting the contrast between company-level strengths and sector-wide uncertainty.

Against this backdrop of healthcare job losses and economic concerns, we’ll examine how these developments influence Tenet Healthcare’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

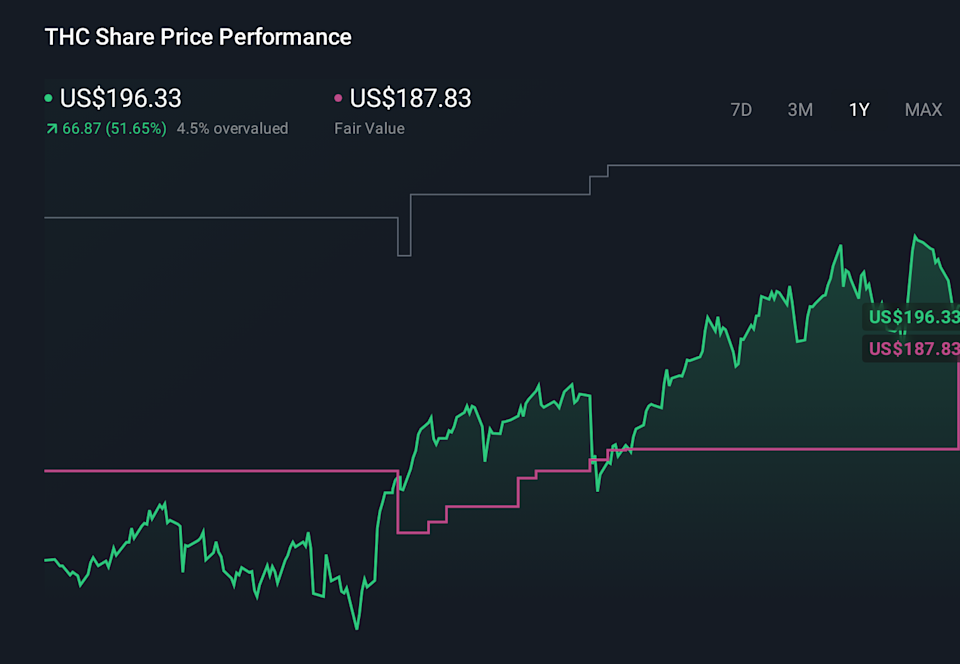

For anyone considering Tenet Healthcare, the core belief is that its mix of acute hospitals, the large United Surgical Partners ambulatory platform and an offshore services engine can keep generating solid cash flows despite a slower growth profile and a high debt load. The stock has run very hard over the past year, supported by consistent earnings beats, buybacks and upbeat 2026 guidance, even as full year 2025 profit margins compressed and earnings declined. Consensus and community valuations still sit above the current price, but the February jobs report and associated share pullback highlight how quickly sentiment can swing when macro worries flare up. For now, those employment data points look more like a sentiment headwind than a thesis changer, although they sharpen the focus on volume resilience and pricing at a time when analysts expect only modest revenue growth and lower earnings ahead.

However, the combination of high leverage and softer profit trends is something investors should not ignore. Despite retreating, Tenet Healthcare’s shares might still be trading above their fair value and there could be some more downside. Discover how much.

THC 1-Year Stock Price Chart

THC 1-Year Stock Price Chart

Four Simply Wall St Community fair value estimates span roughly US$211 to US$647 per share, reflecting very different expectations. Set against recent macro jitters and Tenet’s debt burden, that spread underlines why it helps to weigh several independent views on how the business might perform.

Explore 4 other fair value estimates on Tenet Healthcare – why the stock might be worth 11% less than the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

We’ve uncovered the 16 dividend fortresses yielding 5%+ that don’t just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include THC.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com