Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

Aveanna Healthcare Holdings is back in focus after the modeled fair value in one analyst framework shifted from $11.00 to $10.25 per share, a change of around 7% in the price target. That new $10.25 level now sits close to the revised average on the Street, where some firms are raising targets while others are cutting them, reflecting a genuinely mixed read on Aveanna’s progress. As you read on, you will see how these shifting targets shape the narrative and what to watch as new research rolls in.

Raymond James recently upgraded Aveanna, which signals that at least one firm sees the risk and reward balance as more attractive at current levels.

Earlier in the year, Barclays, RBC Capital and UBS each lifted their price targets, suggesting these firms see room for value creation if the company executes on its healthcare services model.

BMO Capital trimmed its target by US$1, indicating some caution around how current fundamentals line up with prior expectations.

Truist also reduced its target by US$1, reinforcing that parts of the Street are reassessing assumptions on Aveanna’s execution and growth prospects.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

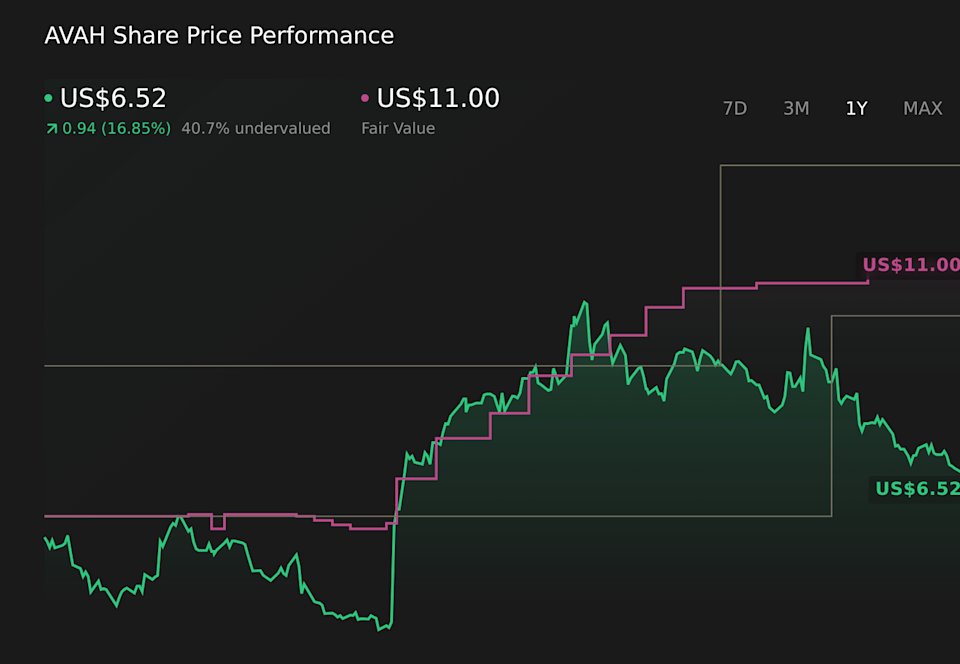

NasdaqGS:AVAH 1-Year Stock Price Chart

NasdaqGS:AVAH 1-Year Stock Price Chart

We’ve flagged 4 risks for Aveanna Healthcare Holdings. See which could impact your investment.

Aveanna maintained earnings guidance for the year ending January 2, 2027, with revenue expected between US$2.54b and US$2.56b, reaffirming its previously communicated range.

For the year ending January 3, 2026, the company issued guidance for revenue of approximately US$2.425b to US$2.445b and projected net income of about US$181m to US$220m.

Alongside the 2026 outlook, Aveanna reiterated its 2027 revenue expectations in a range of US$2.54b to US$2.56b, keeping the long term top line view unchanged.

For 2025, Aveanna updated its earnings guidance to a revenue range of US$2.425b to US$2.445b, compared with earlier commentary that referenced revenue of greater than US$2.375b.

Fair value moved from US$11.00 to US$10.25 per share, a reduction of around 7% in the modeled equity value per share.

Revenue growth assumption adjusted from 6.73% to 5.38%.

Net profit margin assumption reduced from 5.39% to 4.13%.

Future P/E multiple increased from 23.14x to 28.78x.

Discount rate moved from 7.38% to 7.47%.

Story Continues

Narratives link a company’s real world story to a structured forecast and fair value framework so you can see how business trends feed into the numbers. They refresh as new guidance, estimates, and risks are added.

Head over to the Simply Wall St Community and follow the Narrative on Aveanna Healthcare Holdings to stay up to date on:

How demand for in home healthcare and an aging U.S. population are shaping Aveanna’s opportunity set across pediatric and adult services.

The impact of preferred payer agreements, operational efficiency projects, and acquisitions like Thrive Skilled Pediatric on margins and earnings potential.

Key risks around Medicaid and Medicare reimbursement, high variable rate debt, wage inflation, and the rise of technology enabled home healthcare models.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AVAH.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com