On April 9, 2026, Universal Health Services filed a definitive proxy statement urging shareholders to vote against a proposal from investor John Chevedden that would require reporting annual meeting vote results based on the amount of company shareholder money at risk. This governance clash comes as Universal Health Services highlights multi‑year earnings per share growth, aggressive share repurchases, and expansion in behavioral health, raising questions about how voting power and economic exposure should align for investors. Next, we’ll consider how this shareholder voting-rights debate, centered on “money at risk” reporting, may affect Universal Health Services’ investment narrative.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

Universal Health Services Investment Narrative Recap

To own Universal Health Services, you need to believe that its mix of acute and behavioral health assets can convert steady patient demand and operational execution into resilient earnings and cash flow. The immediate catalyst is whether management can keep expanding behavioral health and outpatient volumes while controlling labor costs. The recent proxy fight over “money at risk” vote reporting is unlikely to alter that near term, but it does sharpen attention on governance and long term incentives.

The most relevant backdrop to this governance dispute is UHS’s February 2026 update, highlighting 2025 diluted EPS of US$23.10 and continued share repurchases under its multiyear buyback authorization. Those results frame why questions about how voting power aligns with actual capital at risk matter, especially as UHS leans on buybacks and behavioral health expansion as key supports for earnings per share amid reimbursement and staffing pressures.

Yet even with solid recent EPS and ongoing buybacks, investors should be aware that rising labor and reimbursement pressures could still…

Read the full narrative on Universal Health Services (it’s free!)

Universal Health Services’ narrative projects $20.4 billion revenue and $1.5 billion earnings by 2029. This requires 5.5% yearly revenue growth with earnings remaining flat from $1.5 billion today.

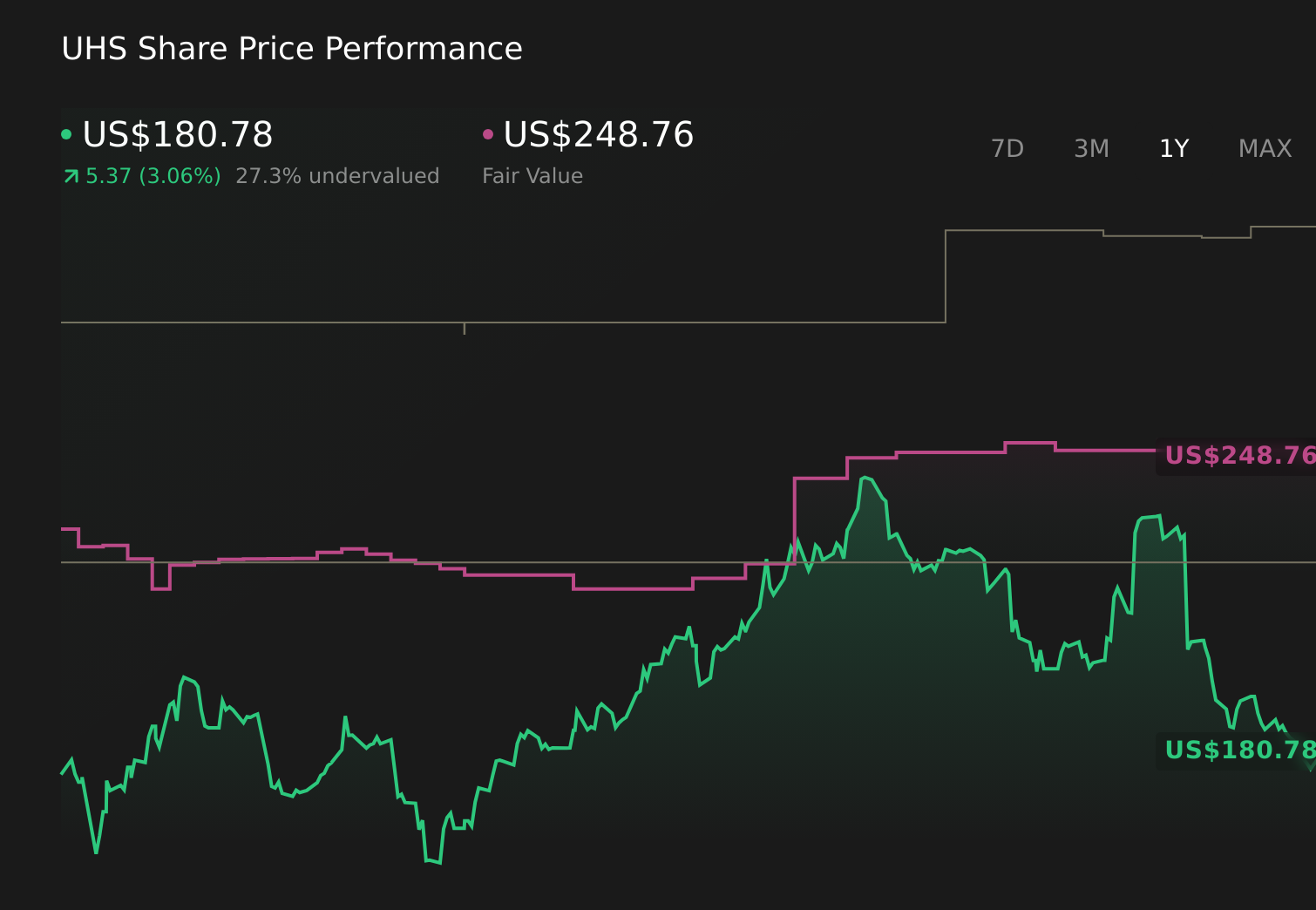

Uncover how Universal Health Services’ forecasts yield a $248.76 fair value, a 38% upside to its current price.

Exploring Other Perspectives UHS 1-Year Stock Price Chart

UHS 1-Year Stock Price Chart

While consensus focuses on growth in behavioral health and buybacks, the most pessimistic analysts already expected only about US$19.0 billion of revenue and US$1.4 billion of earnings by 2028, so you should consider whether the new voting rights dispute reinforces those concerns about long term margin pressure and payor risk.

Explore 3 other fair value estimates on Universal Health Services – why the stock might be worth just $224.48!

Form Your Own Verdict

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Interested In Other Possibilities?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com