Grindr (GRND) recently launched Out in the Open, a Grindr for Equality content series on chemsex, addiction, and mental health, integrating support resources from partners like You Are Loved and Switchboard directly into its app.

See our latest analysis for Grindr.

Alongside this new Grindr for Equality initiative, the stock has shown gaining momentum, with a 10.87% 90 day share price return and a 109.40% three year total shareholder return, despite a 30.78% total shareholder return decline over the past year.

If social impact stories like Grindr’s have your attention, it could be a good moment to broaden your watchlist with 19 top founder-led companies

With shares at $13.36, annual revenue of $439.898 and net income of $84.846, along with an analyst price target of $18.00 and an indicated intrinsic discount of 60.33%, is Grindr undervalued or already pricing in future growth?

Most Popular Narrative: 25.8% Undervalued

With Grindr at $13.36 and the most followed narrative pointing to a fair value of $18.00, analysts see a meaningful gap between price and their model.

Ongoing shift toward value-added premium tiers, coupled with planned pricing experiments and the introduction of more differentiated features (e.g., mapping, intentions-based products, A-List), positions Grindr to lift ARPU and improve net margins over time.

Curious what justifies that higher fair value? The narrative leans heavily on faster earnings growth, richer margins, and a future profit multiple above the sector. The exact mix may surprise you.

Result: Fair Value of $18.00 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on costs staying in check and user monetization holding up, as long as regulatory and management change risks do not erode margins or advertiser confidence.

Find out about the key risks to this Grindr narrative.

Another Angle on Valuation

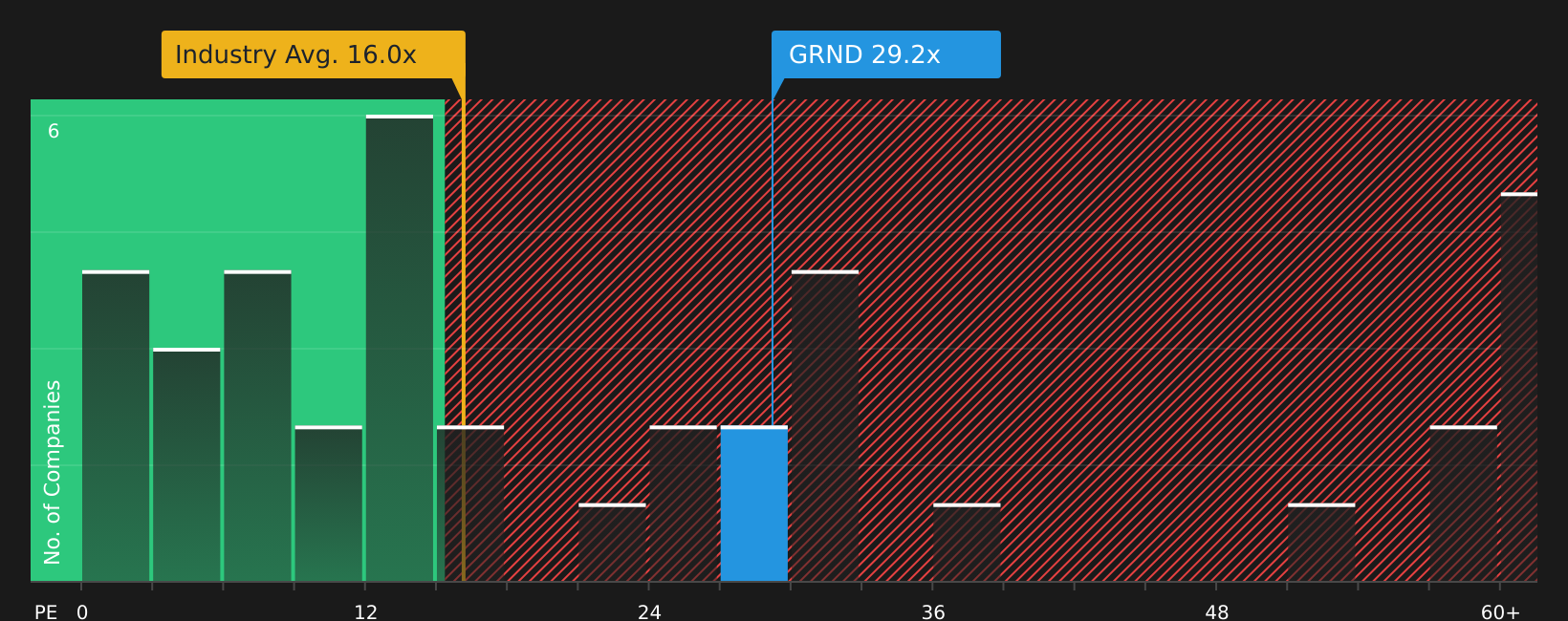

Analysts see Grindr as undervalued at $13.36 versus their $18.00 target, yet the current P/E of 29.2x tells a tougher story. It sits above both the US Interactive Media and Services average of 15.9x and an estimated fair ratio of 21.7x, which points to valuation risk if sentiment cools.

That leaves a clear question for you: is this a case of earnings needing to catch up to the price, or expectations needing to come down? See what the numbers say about this price — find out in our valuation breakdown.

NYSE:GRND P/E Ratio as at Apr 2026Next Steps

NYSE:GRND P/E Ratio as at Apr 2026Next Steps

After considering all of this, are you leaning bullish or cautious on Grindr? Take a closer look at the complete picture of potential upside and downside with 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Grindr is on your radar, do not stop here. Broaden your watchlist now so you are not the one catching up after the next big move appears through the screener.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com