Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

Universal Health Services, Inc. (NYSE:UHS) has opened a new acute care hospital, expanding its service footprint.

The company is increasing investments in behavioral health services to address rising patient demand.

These moves highlight a focus on operational growth beyond quarterly financial figures or guidance.

Universal Health Services enters this expansion phase with its shares at $232.6 and a 1-year return of 28.7%. Over 3 years, the stock is up 61.5%, and over 5 years it has gained 86.7%, which puts recent moves into context for investors tracking the company’s longer-term performance.

For you as a shareholder or potential investor, the new hospital and added behavioral health investment provide a clearer view of how NYSE:UHS is prioritizing growth areas and patient demand. The rest of this article examines what these decisions could mean for capacity, competitive positioning, and how the business is being shaped beyond headline earnings numbers.

Stay updated on the most important news stories for Universal Health Services by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Universal Health Services.

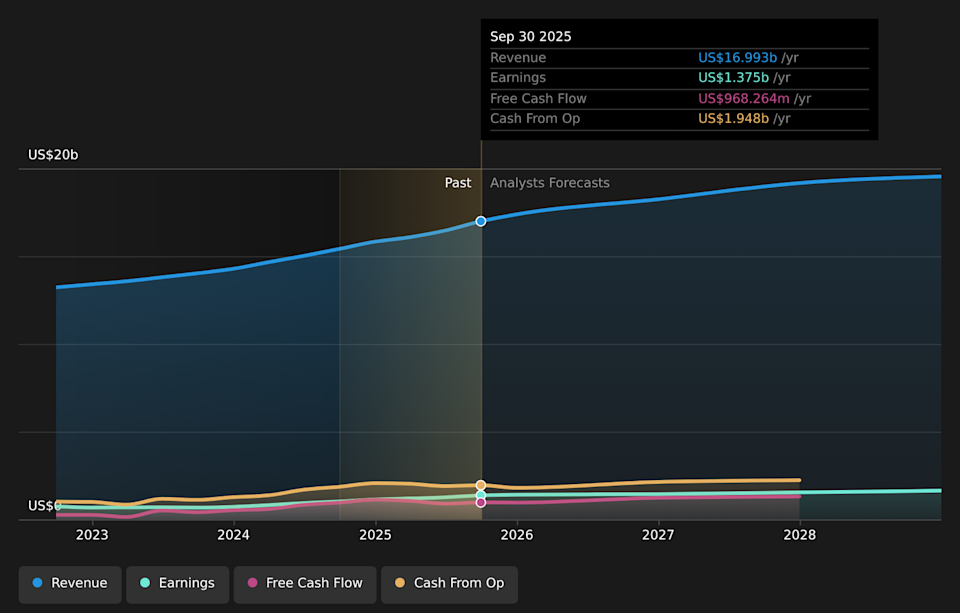

NYSE:UHS Earnings & Revenue Growth as at Feb 2026

NYSE:UHS Earnings & Revenue Growth as at Feb 2026

Beyond the headline: 1 risk and 4 things going right for Universal Health Services that every investor should see.

Beyond the headline: 1 risk and 4 things going right for Universal Health Services that every investor should see.For Universal Health Services, a new acute care hospital plus extra capital going into behavioral health points to a business model that leans into volume and mix rather than one-off financial levers. Acute capacity can support admissions growth in markets where demand is tight, while behavioral health tends to be more recurring and less tied to elective procedures. Together, that can help UHS compete more effectively with large hospital operators such as HCA Healthcare and Tenet Healthcare, which are also active in facility expansion and service line focus. At the same time, management is layering these projects on top of ongoing efficiency initiatives, so execution risk sits in delivering higher throughput without letting labor and supply costs erode the benefits. For you, the key question is whether these added beds and programs translate into sustained patient volumes and a better payer mix, or whether they simply add fixed costs in a sector that already faces reimbursement pressure and staffing constraints.

The new hospital and behavioral health buildout align with the narrative’s focus on expanding behavioral and acute capacity to capture growing demand and support long-term earnings power.

These projects could test the narrative’s concerns about labor shortages and reimbursement risk if higher staffing needs and payor scrutiny offset the benefits of higher volumes.

The current news also touches on operational efficiency efforts, which are mentioned in the narrative, but specific impacts from newer technologies and digital tools may not yet be fully reflected there.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Universal Health Services to help decide what it’s worth to you.

Higher capital and operating commitments for new facilities can pressure returns if patient volumes or reimbursement terms fall short of expectations.

Higher capital and operating commitments for new facilities can pressure returns if patient volumes or reimbursement terms fall short of expectations.

Analysts have flagged at least 1 key risk for UHS, including concerns about the company’s debt levels and how additional investments might affect its financial position.

UHS is growing its acute and behavioral footprint, which aligns with analyst expectations that earnings and revenue can increase over time if demand for these services stays supportive.

UHS is growing its acute and behavioral footprint, which aligns with analyst expectations that earnings and revenue can increase over time if demand for these services stays supportive.

The company is investing into areas where analysts already see rewards, such as earnings growth and what they view as attractive value compared to estimated fair value and peers.

From here, you may want to watch how quickly the new acute care hospital ramps up occupancy and whether behavioral health investments show up in sustained admissions and revenue contributions. Keep an eye on staffing costs and vacancy rates in both segments, since these will indicate whether the added capacity is being supported efficiently. It is also worth tracking upcoming earnings releases and guidance updates to see how management frames the returns on these projects and whether any changes emerge in UHS’s capital allocation, including dividends and buybacks. Any shifts in payer behavior or reimbursement terms, particularly for behavioral programs, will be important signals for how durable the expansion strategy is.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Universal Health Services, head to the community page for Universal Health Services to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include UHS.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com