Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

Analysts have lifted their fair value estimate for BrightSpring Health Services from US$41.93 to US$51.00, and several firms now cluster price targets in a US$48 to US$53 range. That shift comes alongside Q4 updates and the Amedisys/LHC home health and hospice acquisition. Bullish voices see a larger provider and pharmacy footprint as a potential source of incremental growth, while others flag integration and timing risks. As you read on, you will see how this evolving narrative may shape the way investors track BrightSpring from here.

Stay updated as the Fair Value for BrightSpring Health Services shifts by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on BrightSpring Health Services.

Several firms, including Morgan Stanley, Mizuho, UBS, Deutsche Bank and Wells Fargo, have lifted BrightSpring Health Services price targets into a US$48 to US$53 range after Q4, signaling more constructive views on valuation following updated models.

Morgan Stanley and Wells Fargo explicitly factor in the Amedisys/LHC home health and hospice assets and pharmacy contribution, suggesting the enlarged provider and pharmacy platform is central to their investment cases.

Mizuho describes Q4 as “solid” and maintains an Outperform rating, while UBS and Deutsche Bank keep Buy ratings, indicating continued institutional support around the growth story tied to provider services and home health.

Earlier in the year, BTIG, TD Cowen and BMO Capital also raised price targets, adding to a pattern of upward revisions across a broad group of covering analysts.

Mizuho cites physician survey data pointing to decelerating healthcare utilization growth trends, which could cap upside if volumes soften for providers generally, including BrightSpring.

Wells Fargo highlights a tougher setup for hospitals in 2026 and ongoing legislative risk, reminding investors that policy changes and reimbursement pressure remain key execution risks for healthcare services names.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NasdaqGS:BTSG 1-Year Stock Price Chart

NasdaqGS:BTSG 1-Year Stock Price Chart

We’ve flagged 1 risk for BrightSpring Health Services. See which could impact your investment.

BrightSpring Health Services completed a follow on equity offering of 20,000,000 common shares, raising about US$822.7m at roughly US$41.14 per share, after previously filing details of the planned transaction.

The company announced a share repurchase program of up to the lesser of 10% of the shares sold in the offering or US$60m of common stock, with repurchases expected to occur at the same price per share paid by the underwriter and to close together with the offering.

On March 2, 2026, the Board of Directors authorized an additional buyback plan, adding a further capital return option on top of the offering related repurchase authorization.

For Q4 2025, BrightSpring reported impairment of long lived assets of US$6.1m compared with US$5.5m a year earlier, and issued 2026 revenue guidance of US$14.45b to US$15.0b, which it described as 11.9% to 16.2% growth.

Story Continues

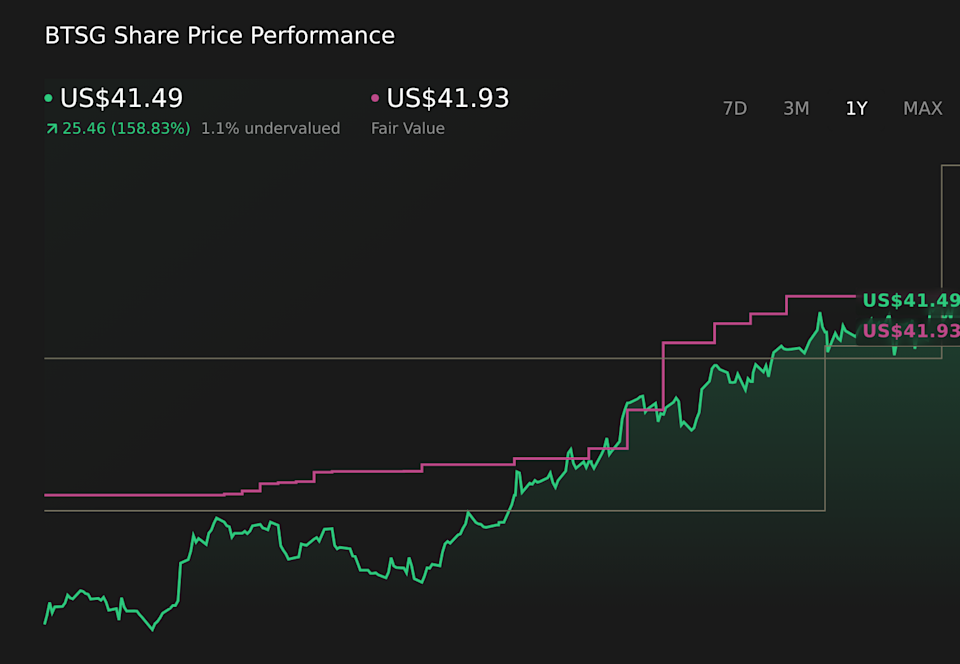

The fair value estimate has moved from US$41.93 to US$51.00 in updated analyst models.

Modeled revenue growth has been adjusted from 12.50% to 13.98% for the forecast period.

The assumed net profit margin has been revised from 2.39% to 2.65% in future years.

The future P/E multiple has shifted from 25.24x to 27.07x in the valuation work.

The discount rate has edged from 6.96% to 6.98% in the latest analysis.

Narratives link a company’s real world story to the financial forecasts and fair value estimates behind it, so you can see why the numbers say what they say. They refresh as new data, guidance, and risks come through.

Head over to the Simply Wall St Community and follow the Narrative on BrightSpring Health Services to stay up to date on:

How growth in specialty pharmacy, rare drug launches, and upcoming exclusives feed into revenue and margin assumptions.

What analysts are building in for home and community based care, demographic aging, acquisitions, and value based care models.

Key risks around labor costs, high leverage, government reimbursement exposure, technology adoption, and rising compliance demands.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BTSG.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com