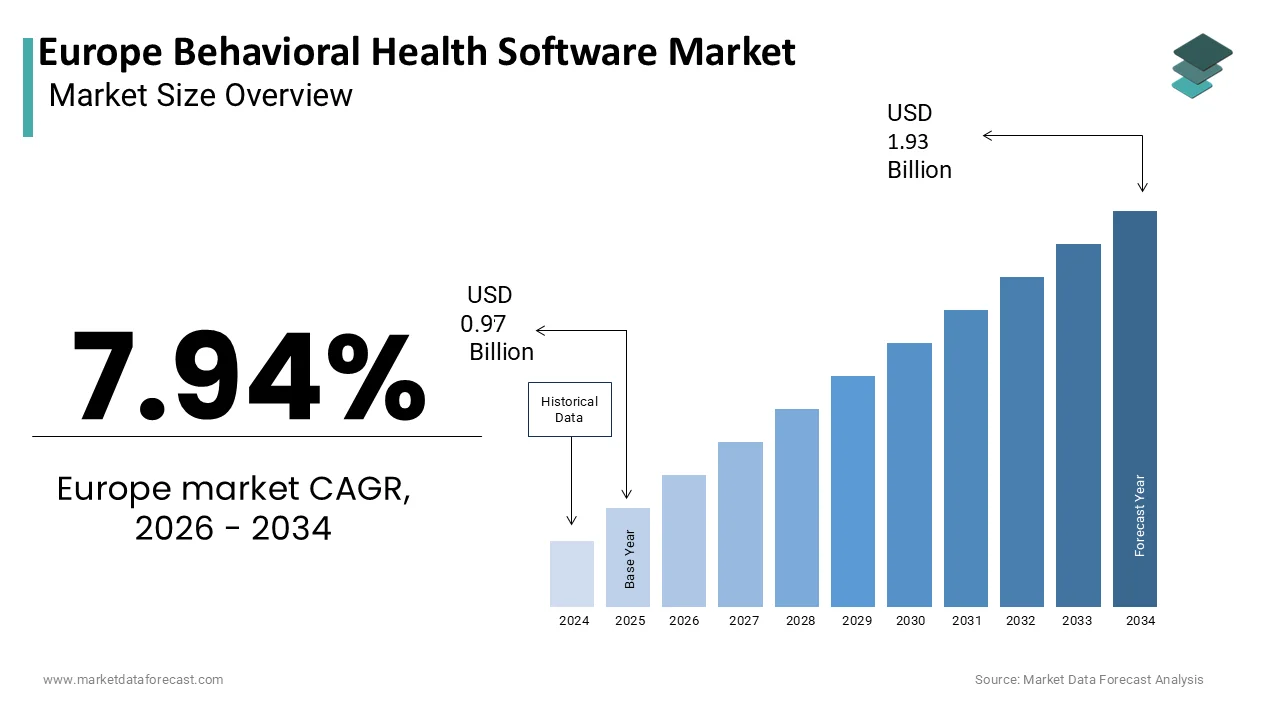

Europe Behavioral Health Software Market Size

The Europe Behavioral Health Software Market was valued at USD 0.97 billion in 2025, is estimated to reach USD 1.05 billion in 2026, and is projected to reach USD 1.93 billion by 2034, growing at a CAGR of 7.94% from 2026 to 2034.

Behavioral health software is a specialized, HIPAA-compliant digital platform designed to manage the unique clinical, administrative, and financial needs of mental health and substance abuse treatment providers. These platforms integrate electronic health records, patient engagement tools, telehealth capabilities, and clinical decision support systems to streamline workflows for psychiatrists, ists psychologists, and counseling centers. The market is defined by its critical role in addressing the escalating prevalence of mental health conditions across the continent while overcoming traditional barriers to care, such as stigma and geographic isolation. According to the WHO Regional Office for Europe, 1 in 6 people in the European Region (approximately 150 million) are now living with a mental health condition. This represents a significant increase from 2019, further intensifying the demand for scalable digital interventions like AI-driven CBT and remote monitoring.

Furthermore, Eurostat data shows that 3.3% of the EU population (roughly 14.7 million people) reported unmet needs for medical examinations in 2023. While lower than 7%, the primary barriers remain “too expensive” or “waiting lists,” areas where digital triage and telehealth platforms are currently being integrated to improve throughput. The European Commission has prioritized mental health in its post-pandemic recovery strategy, emphasizing the integration of digital tools into national healthcare systems. As per the OECD, while the share of mental health spending has reached an average of 3.6% of total health expenditure across Europe, it remains highly skewed. Countries like France and Germany spend closer to 5%, whereas several Eastern European nations remain below 2%, creating a critical “digital bridge” opportunity for cost-effective software solutions. This technological infrastructure supports a shift toward value-based care, enabling providers to track outcomes and deliver personalized treatment plans effectively.

MARKET DRIVERS Rising Prevalence of Mental Health Disorders and Increased Healthcare Spending

The escalating incidence of mental health disorders across the region is a key force behind the growth of the Europe behavioral health software market. The psychological impact of recent global crises, including the pandemic and economic instability, has significantly increased the demand for mental health services. This surge has overwhelmed traditional healthcare infrastructures, necessitating digital solutions that can manage higher patient volumes efficiently. Governments are responding by increasing healthcare budgets allocated to mental health initiatives. For instance, the European Commission launched a comprehensive approach to mental health in June 2023 with an initial investment of 1.23 billion euros to support member states in transforming their mental health systems. This funding encourages the deployment of digital tools that enhance accessibility and continuity of care. Additionally, national health services in countries like the United Kingdom and Germany are integrating digital therapeutics into standard care pathways. The correlation between increased disorder prevalence and governmental financial commitment creates a robust environment for software vendors to expand their offerings and capture growing demand.

Government Initiatives Promoting Digital Health Integration and Telemedicine

Strategic government initiatives aimed at modernizing healthcare infrastructure through digitalization are greatly propelling the Europe behavioral health software market. European policymakers recognize that digital health solutions are essential for achieving universal health coverage and improving service efficiency. The European Health Data Space regulation proposed by the European Commission aims to empower individuals through better control over their health data while facilitating cross-border healthcare services. This regulatory framework supports the interoperability of behavioral health software, allowing seamless data exchange between providers and patients. According to the European Observatory on Health Systems and Policies,s many member states have implemented national eHealth strategies that prioritize telemedicine and remote patient monitoring. For example, France’s Ma Santé 2022 plan includes substantial investments in digital tools to improve access to psychiatric care in underserved rural areas. Similarly, the German Digital Healthcare Act allows physicians to prescribe digital health applications, including those for mental health, which are reimbursed by statutory health insurance. These policy-driven mandates reduce adoption barriers and provide financial incentives for healthcare providers to implement advanced software solutions, thereby accelerating market growth.

MARKET RESTRAINTS Stringent Data Privacy Regulations and Compliance Complexities

The rigorous regulatory landscape governing data privacy in the region constrains the growth of the Europe behavioral health software market. The General Data Protection Regulation imposes strict requirements on the processing of sensitive personal data, which includes mental health information. Compliance with these regulations requires software vendors to implement robust security measures,s encryption protocols, ls and consent management systems, ems which increase development costs and time to market. According to the European Data Protection Board, violations of GDPR can result in fines of up to 20 million euros or 4 percent of global annual turnover,r whichever is higher. This high penalty risk makes healthcare providers cautious about adopting new digital platforms that may not fully comply with legal standards.

Furthermore, the cross-border nature of cloud computing complicates data sovereignty issues as patient data must often remain within European jurisdictions. The ENISA Threat Landscape 2025 highlights that healthcare remains a critical target. Ransomware now accounts for 54% of threats in the sector, with hospitals being the most affected entity (42% of incidents). Financially motivated extortion is the primary driver of these attacks. These security concerns hinder trust among patients and practitioners alike. The complexity of navigating varying national interpretations of GDPR across different member states adds another layer of difficulty for software developers. So, many smaller vendors struggle to meet these compliance demands, limiting market competition and slowing the introduction of innovative solutions.

Fragmented Healthcare Systems and Interoperability Challenges

The fragmentation of healthcare systems across the countries in the region is a major obstacle to the seamless integration of behavioral health software, which hinders the expansion of the Europe behavioral health software market. Each member state operates under a distinct healthcare model,s reimbursement structures, es and IT infrastructure standards, rds which complicates the deployment of unified software solutions. According to the European Observatory on Health Systems and Policies,cies there is significant variation in the maturity of eHealth adoption among EU countries, with Northern and Western nations generally more advanced than Southern and Eastern regions. This disparity creates challenges for software vendors who must customize their products to meet diverse local requirements,ements increasing operational costs. Interoperability remains a critical issue as many existing hospital information systems lack standardized interfaces for connecting with specialized behavioral health platforms.

Contrary to older 50% benchmarks, the average composite score for citizen access to electronic health records in the EU reached 83% in 2024. However, barriers remain in specific data types; for instance, medical imaging is only available for electronic exchange in 26% of cases. The absence of common data standards hinders the ability of software to aggregate and analyze patient information across different care settings. Furthermore, her resistance to change among healthcare professionals who are accustomed to legacy systems slows down adoption rates. These structural and technical barriers prevent the realization of economies of scale and limit the potential for widespread market penetration across the continent.

MARKET OPPORTUNITIES Integration of Artificial Intelligence for Personalized Treatment Plans

The integration of artificial intelligence and machine learning into behavioral health software offers substantial opportunities for enhancing patient outcomes and operational efficiency, which is anticipated to contribute to the growth of the Europe behavioral health software market. AI algorithms can analyze vast amounts of clinical data to identify patterns, predict relapse risks,pse risks, and recommend personalized treatment interventions. Leading psychiatric and digital health researchers are increasingly exploring AI-driven tools, such as chatbots for cognitive behavioral therapy and predictive analytics for suicide prevention, to expand the reach of mental healthcare. These technologies enable early intervention and continuous monitoring, which are crucial for managing chronic mental health conditions. The European Commission’s Horizon Europe program has allocated significant funding for research into AI for health, encouraging innovation in this sector. As per a study published by The Lancet D, AI-basedealth AI-based interventions have shown comparable efficacy to face-to-face therapy for certain conditions, such as depression and anxiety. This evidence supports the clinical validity of digital tools and encourages their adoption by healthcare providers.

Furthermore, the AI can automate administrative tasks such as scheduling and billing, ng freeing up clinicians to focus on patient care. The ability to deliver scalable, cost-effective mental health support through AI-powered platforms addresses the shortage of mental health professionals in many European regions. This technological advancement positions software vendors to offer high-value solutions that transform traditional care delivery models.

Expansion of Remote Patient Monitoring and Mobile Health Applications

The growing acceptance of remote patient monitoring and mobile health applications provides a lucrative possibility for the expansion of the Europe behavioral health software market. Patients increasingly prefer the convenience and anonymity offered by digital platforms for managing their mental well-being. Eurostat shows that more than half of the population across the European Union now uses the internet to find health-related information, reflecting a growing comfort with digital health tools. Mobile apps equipped with mood tracking, meditation guides,s and crisis support features empower patients to take an active role in their recovery. Studies report a steady rise in the availability of mobile health applications, with mental health services emerging as a primary category for new digital developments. Reimbursement policies are also evolving to cover digital therapies,c s as seen in Germany’s DiGA framework, which allows doctors to prescribe approved health apps. Under the Digital Healthcare Act, the German government has authorized several dozen digital health applications for national reimbursement, significantly increasing patient access to regulated digital therapies. This regulatory precedent encourages other European countries to adopt similar frameworks, creating a favorable market environment. Software vendors can capitalize on this trend by developing user-friendly and clinically validated mobile solutions that integrate with existing electronic health records. The shift toward patient-centric care models further drives demand for tools that facilitate continuous engagement and support outside clinical settings.

MARKET CHALLENGES Reimbursement Uncertainties and Fragmented Funding Models

Uncertainty in reimbursement policies and fragmented funding models are major challenges to the European behavioral health software market. Consequently, establishing commercial viability for these digital tools is difficult. Unlike pharmaceutical products, digital health solutions often lack clear pathways for reimbursement from public and private insurers. Reimbursement for digital therapeutics in Europe is highly fragmented, ranging from established statutory tracks to temporary pilot funding, creating disparities in adoption. This inconsistency creates financial barriers for patients and reduces the incentive for healthcare providers to adopt these technologies. In many cases,s patients must pay out of pocket for digital mental health services, es which limits accessibility,ity particularly in lower-income populations. As per sources, out-of-pocket expenditure for mental health care remains high in several European countries, discouraging the use of non-reimbursed digital tools. The lack of standardized health technology assessment frameworks for digital solutions further complicates the approval process for reimbursement. Vendors face lengthy and costly evaluation procedures to demonstrate clinical and economic value to payers.

Furthermore, the rapid pace of technological innovation often outpaces the ability of regulatory bodies to update reimbursement guidelines. This lag creates a mismatch between available technologies and funded services, hindering market growth. Behavioral health software providers are looking at a shaky future. They need unified European reimbursement rules to ensure long-term financial sustainability.

Shortage of Skilled Professionals and Digital Literacy Gaps

The shortage of skilled mental health professionals and varying levels of digital literacy among both providers and patients is a formidable challenge to the Europe behavioral health software market. While software can augment care, it cannot replace the need for trained clinicians to interpret data and provide therapeutic interventions. This workforce gap limits the capacity of healthcare systems to utilize digital tools effectively, as there are insufficient staff to manage the increased patient flow generated by accessible platforms. Additionally, older healthcare providers may lack the digital skills required to operate complex software systems, leading to resistance and low adoption rates. On the patient side, elderly individuals and those from lower socioeconomic backgrounds may struggle to access or navigate digital platforms, exacerbating health inequalities. Addressing these human capital challenges requires substantial investment in education and training programs,ograms which may slow down the immediate uptake of behavioral health software solutions.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

Segments Covered

By Software Type, Deployment Mode, End User, and Region.

Various Analyses Covered

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities

Countries Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe

Market Leaders Profiled

Oracle Corporation (Cerner Corporation), Epic Systems Corporation, Netsmart Technologies, Inc., Qualifacts Systems, Inc., Core Solutions, Inc., Meditab Software, Inc., Holmusk, Welligent, Inc., NextGen Healthcare, Inc., Advanced Data Systems Corporation, Mindable Health GmbH, TELUS Health

SEGMENTAL ANALYSIS By Software Type Insights

The clinical workflow management segment held the majority share of 38.5% of the Europe behavioral health software market in 2025. This supremacy of the segment is largely credited to the critical need for healthcare providers to streamline administrative tasks and ensure accurate documentation amidst rising patient volumes. Behavioral health practices often struggle with complex billing coding and scheduling requirements that differ from general medical practices. Clinical workflow software automates these processes,ocesses reducing administrative burden and minimizing errors. Furthermore, the integration of electronic health records with workflow tools ensures that clinicians have immediate access to patient history treatm, treatment plans, and medication lists. The regulatory requirement for detailed record keeping under the General Data Protection Regulation also necessitates robust workflow management systems that ensure compliance and data security. These platforms facilitate seamless communication between multidisciplinary teams, including ps,ychiatrists p psychologists,s and social workers,s enhancing coordinated care. The ability to generate automated reports for insurance claims and regulatory bodies further drives adoption. Consequently, the operational efficiency and compliance benefits provided by clinical workflow management software make it the most widely adopted solution type in the European market. A top factor for the dominance of the clinical workflow management segment is the stringent regulatory environment and the pressing need for administrative efficiency in European healthcare systems. Behavioral health providers must adhere to strict documentation standards to qualify for reimbursement and maintain legal compliance. Clinical workflow software ensures that all patient interactions, treatments, and outcomes are recorded accurately and securely. Automated workflow systems reduce this risk by validating data entry in real time and flagging potential compliance issues. The General Data Protection Regulation mandates rigorous protection of sensitive mental health data, requiring software that offers advanced encryption and access controls. Additionally, the shortage of administrative staff in many European countries exacerbates the need for automation. Workflow management tools handle appointment scheduling,g reminder notification, and billing process, es freeing up human resources for higher-value tasks. The International Labour Organization notes that automation can mitigate labor shortages by improving productivity per employee. These factors combine to make clinical workflow management an indispensable tool for behavioral health practices seeking to operate efficiently and compliantly in a complex regulatory landscape.

The telehealth segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 24.5% from 2026 to 2034, owing to the permanent shift in patient and provider preferences toward remote care models following the pandemic. Telehealth platforms enable virtual consultations and therapy sessions, on-site and psychiatric evaluations, removing geographic and temporal barriers to access. This trend is particularly pronounced in behavioral health, where stigma and mobility issues often prevent patients from seeking personal care. The European Commission has actively supported the expansion of telehealth through funding initiatives and regulatory frameworks that facilitate cross-border digital health services. The convenience of accessing care from home encourages higher treatment adherence and engagement.

Furthermore t, he integration of telehealth with mobile health applications allows for continuous monitoring and support between sessions. This holistic approach improves patient outcomes and satisfaction. The scalability of telehealth platforms also addresses the shortage of mental health professionals in rural and underserved areas. As digital infrastructure improves and reimbursement policies evolve to cover virtual visits, the demand for telehealth software will continue to surge, driving robust market expansion. The main factor for the rapid growth of the telehealth segment is the improved access to care and the strong patient preference for convenience and privacy. Many individuals with mental health conditions face significant barriers to traditional care , including long waiting times, limited transportation difficulties, and fear of stigma. Telehealth software eliminates these obstacles by allowing patients to connect with providers from the comfort and privacy of their own homes. The anonymity provided by virtual platforms reduces the perceived stigma associated with visiting a mental health clinic. Additionally,nally telehealth enables continuity of care for patients who travel or relocate, ensuring that they do not experience disruptions in treatment. A source highlights that telehealth reduces the risk of infection transmission, which remains a concern for vulnerable populations.

Furthermore,thermore the ability to schedule appointments outside of standard business hours accommodates working professionals and students. This flexibility enhances treatment adherence and reduces dropout rates. Healthcare systems are striving to make mental health services more accessible and patient-centric. Thus, the adoption of telehealth software will continue to accelerate.

By Deployment Mode Insights

cloud-based segment led the Europe behavioral health software market and captured a 62.8% share in 2025. This leading position of the segment is supported by the scalability, cost-effectiveness, and accessibility offered by cloud computing infrastructure. Cloud-based solutions eliminate the need for expensive on-premises hardware and maintenance, allowing healthcare providers to subscribe to software services on a pay-as-you-go basis. Cloud platforms enable seamless access to patient data from any location, facilitating remote work and collaboration among multidisciplinary teams. This flexibility is crucial for behavioral health practices that may operate across multiple sites or offer telehealth services. A study shows that cloud-based software reduces IT operational costs compared to on-premises solutions.

Furthermore, cloud providers invest heavily in security and compliance, ensuring that sensitive patient data is protected according to General Data Protection Regulation standards. Regular automatic updates ensure that software remains current with the latest features and regulatory requirements without disrupting clinical operations. The ability to scale resources up or down based on demand allows practices to manage fluctuating patient volumes efficiently. These operational and financial advantages make cloud-based deployment the preferred choice for the majority of behavioral health software users in Europe. A main fuel for the dominance of the cloud-based segment is the superior cost efficiency and scalability it provides to behavioral health providers. Traditional on-premises software requires significant upfront capital investment in servers, networking equipment,t and specialized IT staff.

In contrast, cloud-based solutions operate on a subscription model, converting capital expenditure into predictable operational expenditure. The scalability of cloud platforms allows practices to add new users or features instantly as their business grows without the need for hardware upgrades. This agility is essential in a dynamic healthcare environment where patient demand can fluctuate rapidly. As per studies, cloud computing enables better resource utilization and energy efficiency,y contributing to sustainability goals. Cloud providers also offer robust disaster recovery and backup services, es ensuring data integrity and business continuity in the event of system failures or cyberattacks. Research emphasizes that reputable cloud providers often have stronger security postures than individual healthcare organizations can afford to maintain. Furthermore, ore the ease of integration with other digital health tools,s such as mobile apps and wearable devices, is enhanced by cloud architecture. These benefits collectively drive the widespread adoption of cloud-based behavioral health software across Europe.

The cloud-based segment is expected to exhibit a noteworthy CAGR of 22.8% during the forecast period, owing to the accelerating digital transformation of healthcare systems and the increasing reliance on remote care models. Moreover, the pandemic catalyzed cloud adoption,n forcing many providers to transition from legacy-premises systems to flexible cloud platforms. The need for real-time data sharing and collaboration among dispersed healthcare teams further fuels this trend. Cloud-based software facilitates seamless integration with telehealth platforms, enabling secure video consultations and remote patient monitoring. The ability to access patient records securely from any device supports the growing trend of mobile healthcare professionals and home-based care services.

Furthermore, advancements in cloud security technologies have alleviated previous concerns about data privacy and sovereignty. The European Data Protection Board has issued guidelines that clarify the compliant use of cloud services for health data, encouraging greater adoption. As healthcare providers continue to prioritize flexibility,y cost savings, and interoperability, the demand for cloud-based oral health software will remain strong. This sustained momentum ensures that the cloud segment outpaces other deployment modes in terms of growth rate. A major push for the rapid growth of the cloud-based segment is its inherent ability to support interoperability and seamless integration with broader digital health ecosystems. Modern healthcare relies on the exchange of data between various systems, including electronic health records, laboratory information systems, and patient portals. Cloud-based platforms utilize standardized application programming interfaces that facilitate this data exchange more effectively than siloed on-premises solutions. Behavioral health software deployed in the cloud can easily integrate with general medical records, ensuring that mental health conditions are treated holistically alongside physical health issues. The cloud also supports the integration of artificial intelligence and analytics tools that require vast computational power and large datasets. These advanced capabilities enable predictive modeling and personalized treatment recommendations that enhance clinical outcomes.

Furthermore, the cloud facilitates the deployment of mobile health applications that sync data in real time with the central platform. This connectivity empowers patients to engage actively in their care journey. The European healthcare landscape is becoming increasingly digitized and interconnected. As a result, cloud-based software is becoming the foundational infrastructure for integration, driving significant market growth.

By End User Insights

The hospitals segment dominated the Europe behavioral health software market and accounted for a 45.7% share in 2025. This dominance of the segment is driven by the high volume of patients treated in hospital settings and the complexity of managing behavioral health services within large healthcare institutions. Hospitals often have dedicated psychiatric wards and outpatient clinics that require sophisticated software solutions for patient management, billing, a nd clinical documentation. The integration of behavioral health software with existing hospital information systems ensures seamless data flow and coordinated care across departments. Hospitals also benefit from economies of scale when implementing enterprise-wide software solutions, making them attractive customers for vendors. The regulatory requirements for reporting and quality assurance in hospital settings further drive the adoption of comprehensive software platforms. These systems enable hospitals to track key performance indicators, monitor patient outcomes, and ensure compliance with national standards. The financial resources available to large hospital networks also allow for significant investment in advanced technologies. Consequently, the hospitals segment remains the largest end user group in the European behavioral health software market. A key factor sustaining the dominance of the hospitals segment is the strategic shift toward integrating behavioral health services with general health care,e to provide comprehensive care models. Comorbidity between mental and physical health conditions is common, requiring coordinated treatment approaches. Hospitals are at the forefront of this integration, utilizing software to manage complex patient cases that involve multiple specialties. Behavioral health software in hospitals facilitates communication betweenpsychiatrists,s primary care physicians,ans and other specialists, ensuring that treatment plans are aligned. The software enables the sharing of critical information such as medication lists and allergy alerts, reducing the risk of adverse drug interactions

Furthermore, more hospitals use these platforms to manage emergency psychiatric presentations,,ons ensuring timely and appropriate interventions. The ability to track patient progress over time and across different care settings enhances the continuity of care. This holistic approach aligns with the European Commission’s goal of person-centered healthcare systems. Hospitals are increasingly adopting integrated care models. This trend ensures a strong, ongoing demand for sophisticated behavioral health software that supports multidisciplinary collaboration.

The counseling centers segment is predicted to witness the highest CAGR of 21.2% between 2026 and 2034. This rapid growth of the segment is supported by the increasing recognition of the importance of early intervention and outpatient care for mental health conditions. Counseling centers often operate with limited resources and staff, making efficient software solutions essential for managing patient loads and administrative tasks. These centers are increasingly adopting cloud-based software to streamline scheduling, billing,g and client management. The affordability and ease of use of modern software platforms make them accessible to smaller practice s.Furthermore, re the rise of telehealth has enabled counseling centers to expand their reach beyond llocal communitiesies attracting clients from wider geographic areas. Software that supports secure video conferencing and remote session management is particularly valuable for these providers. The flexibility to scale services based on demand allows counseling centers to grow sustainably. As mental health awareness continues to increase and more individuals seek professional support, port the counseling centers segment will experience sustained high growth rates. The primary factor for the rapid growth of the counseling centers segment is the broader societal shift to community-based and preventive mental health care. European healthcare systems are increasingly prioritizing early intervention and outpatient services to prevent the escalation of mental health issues into severe conditions requiring hospitalization. Counseling centers play a pivotal role in this ecosystem, providing accessible and timely support to diverse populations. Software solutions enable these centers to manage large caseloads efficiently while maintaining high standards of care. The ability to offer flexible appointment scheduling and remote sessions enhances accessibility for working individuals and students.

Furthermore, counseling centers often serve vulnerable groups,s including refugees and of traumaftraumau, ma requiring specialized case management features. Software that supports multilingual interfaces and culturally sensitive care protocols is increasingly in demand. The decentralization of mental health services away from large institutions toward local community hubs creates a vast market for scalable software solutions. Governments and insurers are continuing to fund preventive care initiatives. Thus, the counseling centers segment will remain a key driver of market expansion.

COUNTRY LEVEL ANALYSIS Germany Behavioral Health Software Market Analysis

Germany was the top performer in the Europe behavioral health software market and captured a 22.5% share in 2025. This growth of the German market is fuelled by a robust healthcare infrastructure and a progressive regulatory framework that supports digital health innovation. The German Digital Healthcare Act allows physicians to prescribe digital health applications,ons including those for mental health, all of which are reimbursed by statutory health insurance. According to the Federal Institute for Drugs and Medical Devices (BfArM), the number of approved Digital Health Applications (DiGA) eligible for statutory reimbursement has nearly doubled since the initial phases, establishing a robust and maturing market for prescribed digital therapeutics. The high prevalence of mental health disorders in Germany,rmany coupled with a strong emphasis on data privacy, drives the adoption of secure and compliant software solutions. As per the Robert Koch Institute,stitute one in four adults in Germany experiences a mental disorder in any given year,r highlighting the urgent need for scalable digital interventions. The well-developed IT infrastructure and high internet penetration facilitate the deployment of cloud-based platforms.

Furthermore, the presence of leading technology companies and startups fosters innovation in the behavioral health sector. The German government’s investment in eHealth initiatives,s including the introduction of the electronic patient record,rd further supports market growth. These factors combined ensure that Germany remains the dominant force in the European behavioral health software market.

United Kingdom Behavioral Health Software Market Analysis

The United Kingdom was the second largest country in the Europe behavioral health software market and held a 18.3% share in 2025 because of the National Health Service’s commitment to expanding access to mental health services through digital channels. The NHS Long Term Plan includes significant investments in digital therapeutics and online therapy platforms to reduce waiting times and improve patient outcomes. NHS England reports that hundreds of thousands of patients are now referred to internet-enabled cognitive behavioral therapy (iCBT) pathways annually, reflecting a successful integration of digital tools into the standard care model. The UK has a mature market for behavioral health software with numerous established providers and innovative startups. As per the Office for National Statistics, the prevalence of common mental disorders in the UK has increased,ased particularly among young adults,dults driving demand for accessible care options. The regulatory environment supported by the National Institute for Health and Care Excellence provides clear guidelines for the evaluation and adoption of digital health technolog

es. Furth moreover,,ermore the UK’s strong research base in psychology and psychiatry contributes to the development of evidence-based software solutions. The integration of digital tools into primary care networks ensures that behavioral health services are widely available. The combination of government support, clinical validation,n and high patient demand ensures that the UK remains a key contributor to the European market.

France Behavioral Health Software Market Analysis

France maintains a notable share of the Europe behavioral health software market due to the government’s Ma2022 strategyrategye,gy which prioritizes the digital transformation of the healthcare system. This initiative includes funding for telemedicine and digital health platforms to improve access to care in underserved areas. According to the French Ministry of Solidarity and Health, lth the number of teleconsultations has increased significantly,ntly with mental health being a major component. The French healthcare system is characterized by a mix of public and private provider,s creating a diverse market for software solutions. As per the National Institute of Health and MedicaResearch,ch mental health disorders affect a significant portion of the French population,ulation driving the need for efficient management tools. The regulatory framework is evolving to support the reimbursement of digital therapeutic interventions,ventions although it remains more complex than in Germany. The presence of major technology hubs in Paris and Lyon fosters innovation in health tec

. Furthermore,rthermore the cultural shift toward accepting mental health care is increasing demand for discreet and accessible digital services. The integration of behavioral health software with existing electronic health records is a key focus area for vendors. These strategic developments ensure that France maintains a strong position in the European market.

Italy Behavioral Health Software Market Analysis

Italy is moving ahead steadfastly in the Europe behavioral health software mark et,are market owing to a growing emphasis on modernizing the mental health secor ,which hahistorically community-baseded services. The National Recovery and Resilience Plan allocates substantial funds for digital health infrastructure, including the development of telemedicine platforms. According to the Italian National Institute of Statistics,s the demand for mental health services has risen, en particularlin the post-pandemiccc period. The Italian healthcare system is decentralized, with regions having significant autonomy,y leading to varied adoption rates of digital tools. As per the WorldHealth Organizationi,n Italy has made progress in deinstitutionalizing mental heal h care,are creating opportunities for community-based digital solutions. The increasing penetration of smartphones and internet access facilitates the use of mobile health applications for mental well-being.

Furthermore, the government is working to standardize electronic health records across regions,s which will support the integration of behavioral health software. The presence of innovative startups in Milan and Rome contributes to the development of localized solutions. As Italy continues to invest in digital health and address the mental health needs of its aging population,n the market for behavioral health software is expected to grow steadily.

Spain Behavioral Health Software Market Analysis

Spain is likely to grow notably in the Europe behavioral health software market during the forecast period due to the implementation of the Strategy for Mental Health, which aims to improve access to care and reduce stigma. The Spanish National Health System is increasingly incorporating digital tools to support psychological interventions and patient monitoring. The Ministry of Health acknowledges a persistent and critical shortage of specialized mental health professionals relative to the European average, a gap that is accelerating the adoption of automated and remote software solutions to extend provider capacity. The high rate of internet usage and smartphone penetration in Spain supports the adoption of mobile health applications. Private sector health reports indicate that the rapid growth in telemedicine usage is being disproportionately driven by mental health consultations, as patients seek immediate access to care that is often unavailable through traditional face-to-face channels. The government is promoting the use of digital platforms to reach rural and isolated population

. Furthermore,e the private sector is investing in digital mental health startups offering innovative solutions for anxiety and depression. The regulatory environment is becoming more supportive of digital health innovations with ongoing efforts to establish reimbursement frameworks. The cultural acceptance of mental health care is improving, particularly among younger generations. These factors combined create a conducive environment for the growth of the behavioral health software market in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe behavioral health software market is characterized by a mix of established global vendors and innovative regional startups. Major multinational corporations leverage their extensive product portfolios and financial resources to offer comprehensive end-to-end solutions. These incumbents benefit from strong brand recognition and existing relationships with large healthcare networks. However, specialized startups challenge this dominance by introducing agile and user-friendly platforms that address niche market needs. The market sees frequent innovation as companies strive to differentiate themselves through advanced features such as artificial intelligence-driven insights and seamless telehealth integration. Regulatory compliance with the General Data Protection Regulation serves as a critical competitive factor requiring vendors to demonstrate robust data security measures. Companies that successfully balance innovation with compliance gain a strategic advantage in attracting risk-averse healthcare providers. Strategic acquisitions are common as firms seek to expand their technical expertise and geographic footprint. This dynamic environment fosters continuous improvement but also creates pressure on pricing and customer retention. Agility and customer centricity remain essential for sustaining long-term success in this rapidly evolving sector, where trust and reliability are paramount for adoption.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Behavioral Health Software Market include

Oracle Corporation (Cerner Corporation) Epic Systems Corporation Netsmart Technologies, Inc. Qualifacts Systems, Inc. Core Solutions, Inc. Meditab Software, Inc. Holmusk Welligent, Inc. NextGen Healthcare, Inc. Advanced Data Systems Corporation Mindable Health GmbH TELUS Health TOP LEADING PLAYERS IN THE MARKET Infor Inc is a prominent player in the Europe behavioral health software mark et,et offering comprehensive, cloud-based solutions tailored for healthcare providers. The company provides specialized electronic health records and practice management tools that streamline clinical workflows and enhance patient engagement. Infor recently strengthened its market position by enhancing its artificial intelligence capabilities within its CloudSuite Healthcare platform to support predictive analytics for mental health outcomes. These innovations help European hospitals and clinics optimize resource allocation and improve care coordination. The company’s global contribution includes setting standards for interoperability and data security in behavioral health IT. Infor actively collaborates with European healthcare institutions to ensure compliance with local regulations such as the General Data Protection Regulation. By focusing on user-friendly interfaces and robust integration features, Infor enables providers to deliver high-quality mental health services efficiently. Its commitment to innovation and customer success ensures that it remains a trusted partner for healthcare organizations seeking to modernize their behavioral health infrastructure. Netsmart Technologies significantly influences the Europe behavioral health software market through its myEvolv and CarePort platforms, which support integrated care delivery. The company specializes in solutions for community-based behavioral health organizations, enabling seamless coordination between physical and mental health services. Netsmart recently expanded its European presence by partnering with local health systems to implement value-based care models supported by advanced data analytics. These initiatives help providers track patient outcomes and demonstrate efficacy to payers and regulators. Globally, Netsmart contributes by promoting the of person-centered careteredcare technologies that empower individuals to manage their own health. The company invests heavily in research and development to incorporate telehealth and remote monitoring features into its software suite. This focus on accessibility aligns with European healthcare priorities for expanding mental health access. Netsmart’s emphasis on interoperability ensures that its solutions integrate smoothly with existing hospital information systems. Netsmart drives the transformation of behavioral healthcare across diverse settings. They achieve this by delivering secure, scalable technology platforms. Qualifacts Systems Inc plays a crucial role in the Europe behavioral health software market by providing enterprise-grade solutions for large healthcare networks. The company offers CareLogic and Credible platforms, which are widely used for managing complex behavioral health cases and ensuring regulatory compliance. Qualifacts recently strengthened its position by acquiring complementary technology firms to expand its portfolio of revenue cycle management and clinical documentation tools. These acquisitions enable the company to offer end-to-end solutions that reduce administrative burdens for providers. Globally, Qualifacts contributes by establishing best practices for data standardization and security in behavioral health IT. The company works closely with European clients to customize its platforms for local workflow requirements and legal frameworks. Qualifacts prioritizes innovation by integrating artificial intelligence for automated coding and risk assessment. This technological advancement helps providers improve accuracy and efficiency in billing and clinical decision-.making Qualifacts prioritizes operational excellence and client support. This ensures healthcare organizations effectively navigate complex behavioral health management. TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe behavioral health software market primarily focus on strategic partnerships and collaborations to enhance their technological capabilities and expand market reach. Companies frequently join forces with local healthcare providers and technology firms to co-develop solutions tailored to specific regional needs. Another major strategy involves significant investment in research and development to integrate artificial intelligence and machine learning into their platforms. These advancements enable predictive analytics and personalized care planning, which are critical for improving patient outcomes. Market participants also emphasize compliance with European data protection regulations to build trust and ensure seamless market entry. They prioritize interoperability by adopting standardized data formats that facilitate integration with existing hospital systems. Additionally, our companies are expanding their cloud infrastructure to support scalable and secure service delivery. Marketing strategies highlight the efficiency and cost savings benefits of digital tools to attract healthcare administrators. These multifaceted approaches enable key players to maintain competitive advantages and drive widespread adoption of behavioral health software solutions across the diverse European healthcare landscape.

MARKET SEGMENTATION

This research report on the europe behavioral health software market is segmented and sub-segmented into the following categories.s

By Software Type

Clinical Workflow Management Telehealth

By Deployment Mode

By End User

Hospitals Counseling Centers

By Country

Germany United Kingdom France Italy Spain Rest of Europe