LifeStance Health Group (LFST) is drawing fresh interest after S&P Dow Jones Indices said the behavioral health provider will join the S&P SmallCap 600, prompting index tracking funds to start buying shares.

See our latest analysis for LifeStance Health Group.

The latest S&P SmallCap 600 announcement comes on top of a 22.92% 30 day share price return and a 16.74% 1 year total shareholder return. This suggests momentum has picked up recently even though longer term returns remain mixed.

If strong interest in behavioral health is on your radar, it can be useful to see what else the market is rewarding in this space, including AI driven care models via 32 healthcare AI stocks

With LifeStance now profitable, showing annual revenue growth of 13.17% and trading at a discount of about 28% to the current analyst price target of US$9.83, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 14.8% Undervalued

With LifeStance Health Group last closing at $7.67 versus a most followed fair value estimate of $9.00, the current setup centers on how much future growth and profitability are already embedded in that gap.

The continued and accelerating demand for mental health services in the U.S. driven by increasing public awareness and access to insurance coverage is expected to expand LifeStance’s addressable market and support sustained double digit revenue growth in the coming years. The ongoing migration of patients from cash pay to commercial insurance, along with policy initiatives supporting mental health parity, positions LifeStance to benefit from more stable reimbursement streams and higher patient volumes, thus boosting revenue predictability and growth.

Curious what has to happen for that $9.00 fair value to hold up? The narrative focuses on the interaction of faster revenue growth, rising earnings, and a richer future earnings multiple. The full story is in how those three levers are combined and how long the market is assumed to keep paying up for them. Want to see exactly which assumptions carry the most weight in that model?

Result: Fair Value of $9.00 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on insurers holding the line on reimbursement and LifeStance keeping clinicians on board, because pressure on either could quickly weaken that $9.00 narrative.

Find out about the key risks to this LifeStance Health Group narrative.

Another Way To Look At Value

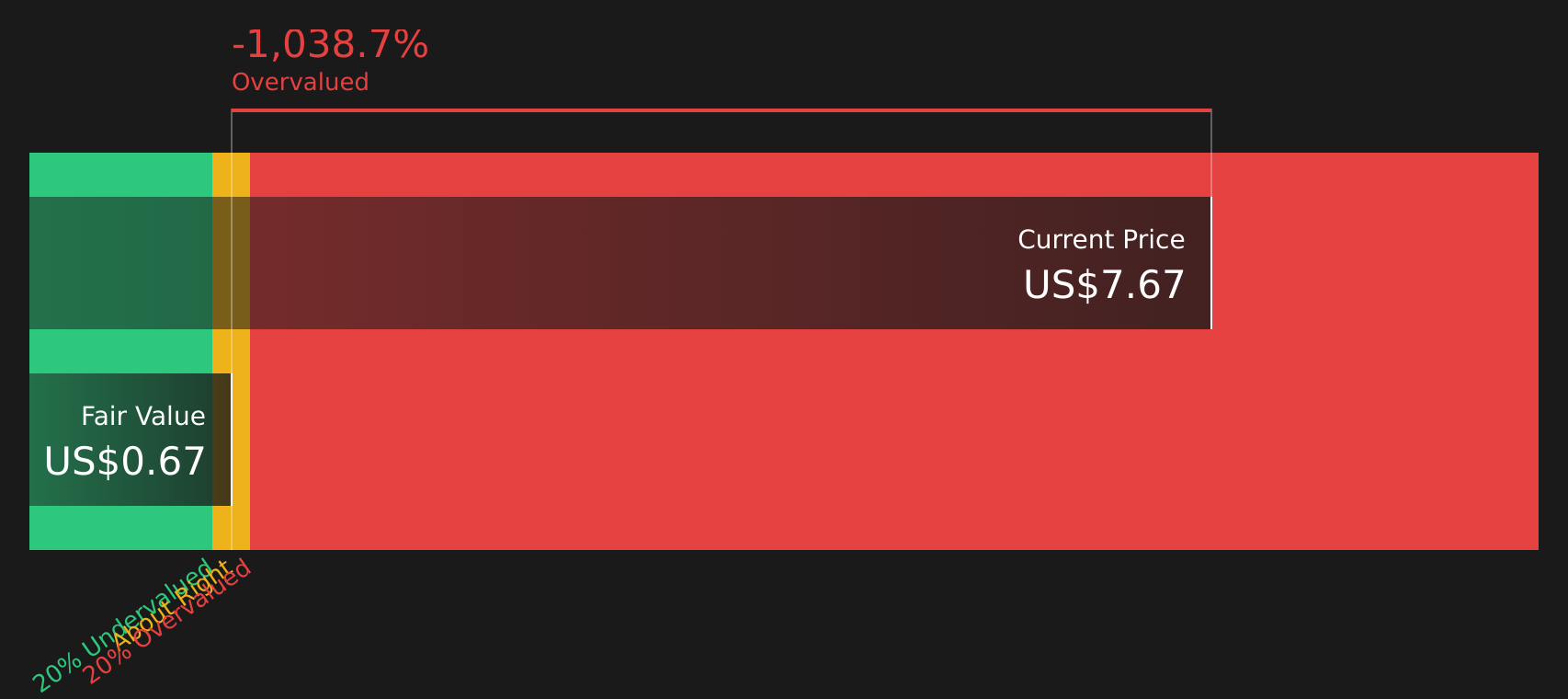

The fair value story built around analyst growth and future earnings multiples runs into a very different signal from the Simply Wall St DCF model, which puts future cash flow value at just $0.67 per share versus the current $7.67 price. That gap suggests investors are paying a lot upfront for growth that may or may not turn into cash. How comfortable are you with that trade off?

Look into how the SWS DCF model arrives at its fair value.

LFST Discounted Cash Flow as at Apr 2026

LFST Discounted Cash Flow as at Apr 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out LifeStance Health Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

Given the mixed signals in this article, it makes sense to look at the underlying data yourself and decide how attractive the setup really feels. To see what investors are currently optimistic about, take a closer look at the 3 key rewards.

Looking for more investment ideas?

If LifeStance has your attention, do not stop here. Give yourself options by lining up a few more ideas that fit your style and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com