Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

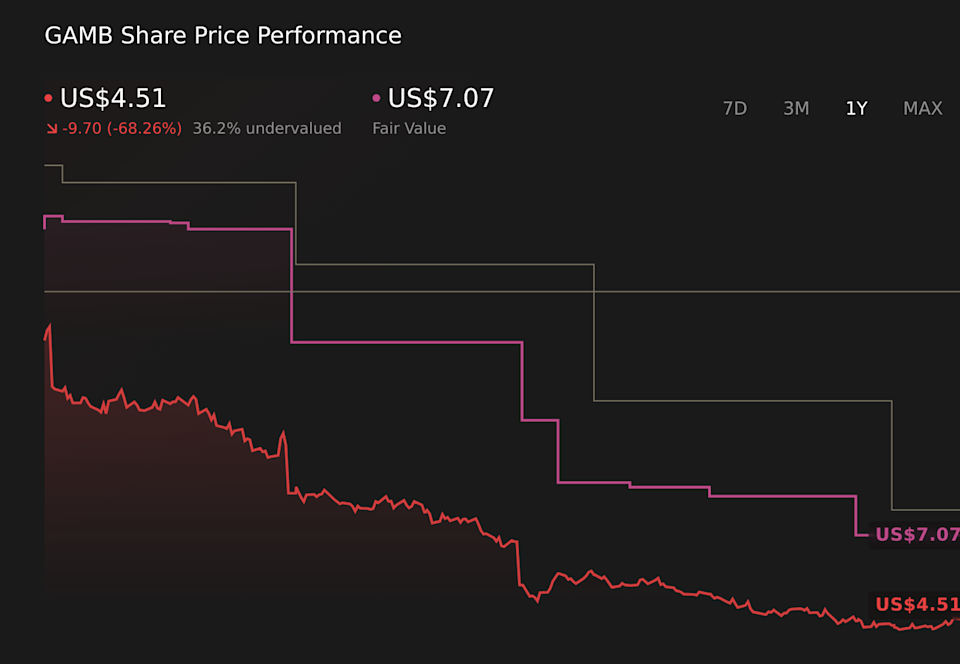

Analysts now reference an implied fair value of US$6.79 for Gambling.com Group, compared with US$7.07 previously, trimming their central valuation mark by about 4%. This shift sits alongside mixed commentary, with bullish voices pointing to an adjusted EBITDA beat and product initiatives. More cautious analysts highlight softer multi year guidance and regulatory pressures as reasons for restraint. Read on to see how to interpret these changing targets and track the evolving narrative around the stock.

Stay updated as the Fair Value for Gambling.com Group shifts by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Gambling.com Group.

What Wall Street Has Been Saying 🐂 Bullish Takeaways

Benchmark, Stifel, Jefferies and Texas Capital all maintain Buy ratings, signaling that several firms still see upside potential despite reduced targets.

Stifel and Benchmark point to a Q4 adjusted EBITDA result that came in modestly above prior consensus, which supports the view that current operations are holding up against headwinds.

Jefferies highlights growth in Sports and flags indications of a new product launch aimed at improving search performance, which some analysts see as a possible support for future execution.

Texas Capital trims its target to US$7.50 from US$9 but keeps a constructive stance, suggesting the stock’s risk reward looks acceptable to that firm at revised levels.

🐻 Bearish Takeaways

Truist cuts its target to US$5 from US$6 and keeps a Hold rating, pointing to FY26 guidance that sits meaningfully below earlier expectations on both revenue and EBITDA.

Across Truist, Benchmark and Stifel, lower FY26 expectations reflect concerns around Google algorithm changes, EU and UK regulatory pressures and marketing headwinds, which collectively weigh on growth assumptions and valuation targets.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NasdaqGM:GAMB 1-Year Stock Price Chart

NasdaqGM:GAMB 1-Year Stock Price Chart

We’ve flagged 1 risk for Gambling.com Group. See which could impact your investment.

What’s in the News

Gambling.com Group plans to put amendments to its Amended and Restated Memorandum and Articles of Association to a shareholder vote at its Annual General Meeting on May 20, 2026.

Founder leadership roles are set to shift after the mid May 2026 Annual General Meeting, with Charles Gillespie becoming Executive Chairman and Kevin McCrystle moving from Chief Operating Officer to Chief Executive Officer.

For 2026, the company issued earnings guidance that includes expected full year revenue of US$170 million to US$180 million, with data services and enterprise sports data services described as key revenue drivers.

For the fourth quarter ended December 31, 2025, Gambling.com Group recorded an impairment loss on intangible assets of US$14,006,000 and reported total share repurchases of 3,960,663 shares, or 10.92% of the company, at a cost of US$35.58 million since November 17, 2022.

Story Continues

How This Changes the Fair Value For Gambling.com Group

Fair value moves from US$7.07 to US$6.79, a reduction of about 4% in the central valuation mark.

Revenue growth assumptions shift from roughly 8.76% to about 7.47% in future models.

Net profit margin assumptions move from about 23.90% to roughly 12.03% of sales.

The assumed future P/E multiple adjusts from about 5.9x to roughly 11.7x.

The discount rate moves from 8.65% to about 8.91% applied to future cash flows.

Never Miss an Update: Follow The Narrative

Narratives connect a company’s business story to a forward looking financial forecast and implied fair value, updating as new data, guidance, and risks come through. They give you one place to track how the thesis is evolving over time.

Head over to the Simply Wall St Community and follow the Narrative on Gambling.com Group to stay up to date on:

How expansion into newly regulated online gambling and sports betting markets, along with the shift to digital first gambling experiences, is shaping Gambling.com Group’s addressable market.

The growing role of higher margin sports data and sports related services, recurring subscriptions, and acquisitions such as Spotlight.Vegas in reshaping the revenue mix.

Key risks around regulation, SEO and search related traffic pressures, rising competition from operators and affiliates, and execution challenges on acquisitions and data services.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include GAMB.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com